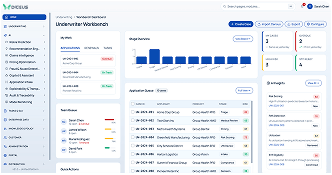

AI-Powered Underwriting Workbench for Health Insurance

Built for underwriting teams that are tired of using a dozen different systems. Everything lives in one place: intake, medical review, pricing, broker communication, decisions, and audit history. Works for both individual and group health insurance.

Book a demo